MEDIA RELEASE

Latest Altron FinTech Household Resilience Index indicates mounting pressure on household finances of South Africans

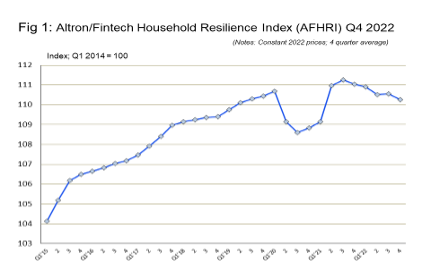

The Index (known as the AFHRI) shows that while household financial resilience increased by 1.4% in the quarter, the decline of 1.1% recorded year-on-year reflects the mounting pressure on household finances.

Johannesburg, 24 April 2023 – The results of the latest quarterly Altron FinTech Household Resilience Index (AFHRI) were released today. After a strong recovery from the effects of the pandemic, which took the index to a record high in the fourth quarter of 2021, the AFHRI has taken a dip, mainly as a result of higher inflation and higher interest rates, which are squeezing the finances of most households.

The MD of Altron FinTech Johan Gellatly says the AFHRI provides valuable insights into the credit sector and is thus considered as a useful benchmark by players in the sector. Altron FinTech uses the information to improve its own understanding of the dynamics of the market which its clients serve so that it designs products and solutions that are both relevant and effective. “Our products and solutions also enable our clients to continue to trade in challenging markets efficiently, which presents a competitive advantage over their peers.”

Background to the AFHRI

In recognition of the need for data that provides more clarity on the financial disposition of households in general, and their ability to cope with debt in particular, Altron FinTech commissioned economist and economic advisor to the Optimum Investment Group, Dr Roelof Botha, to assist in designing this index.

Dr Roelof explains further: “The AFHRI comprises 20 different indicators, all of which are related to sources of income or asset values. The index is weighted according to the demand side of the short-term lending industry and calculated on a quarterly basis, with the first quarter of 2014 being the base period, equalling an index value of 100. All of the indicators are expressed in real terms, i.e., after adjustment for inflation.”

Results for fourth quarter of 2022 explained

Although the index increased marginally from its reading in the third quarter of 2022, it declined by more than 1% compared to the fourth quarter of 2021. Dr Botha explains that due to seasonal volatility related to end-of-year bonuses and the shopping boom associated with Black Friday and Christmas, it is useful to examine the four-year average trend in the index value.

“In the fourth quarter of 2022, the AFHRI recorded a value of 111.5, compared to 109.9 in the third quarter of the same year, and 112.7 in the comparable quarter of 2021. Given the 2014 base level of 100, this means that the average household’s financial disposition has improved by 11.5% in real terms over nine years. However, the average annual improvement since 2014 is only 1.2%, which serves as a clear indication of the economy’s underperformance,” says Dr Botha.

He adds this is especially as a result of the following:

- A decade of state capture and public sector mismanagement between 2009 and 2018 that eroded business confidence and ultimately led to serious infrastructure deficiencies, especially in the areas of energy, roads and railways.

- COVID-19 lockdown regulations, which decimated economic activity in 2020 and led to the loss of more than two million jobs in the space of a single quarter (Q1 2020 to Q2 2020).

- Higher inflation, mainly due to massive increases in freight shipping rates and global supply-side constraints.

- An unwelcome return to restrictive monetary policy by the South African Reserve Bank (SARB), despite the absence of demand inflation. The cost of credit – and of capital – has increased by more than 60% since the SARB started to raise interest rates at the end of 2021.

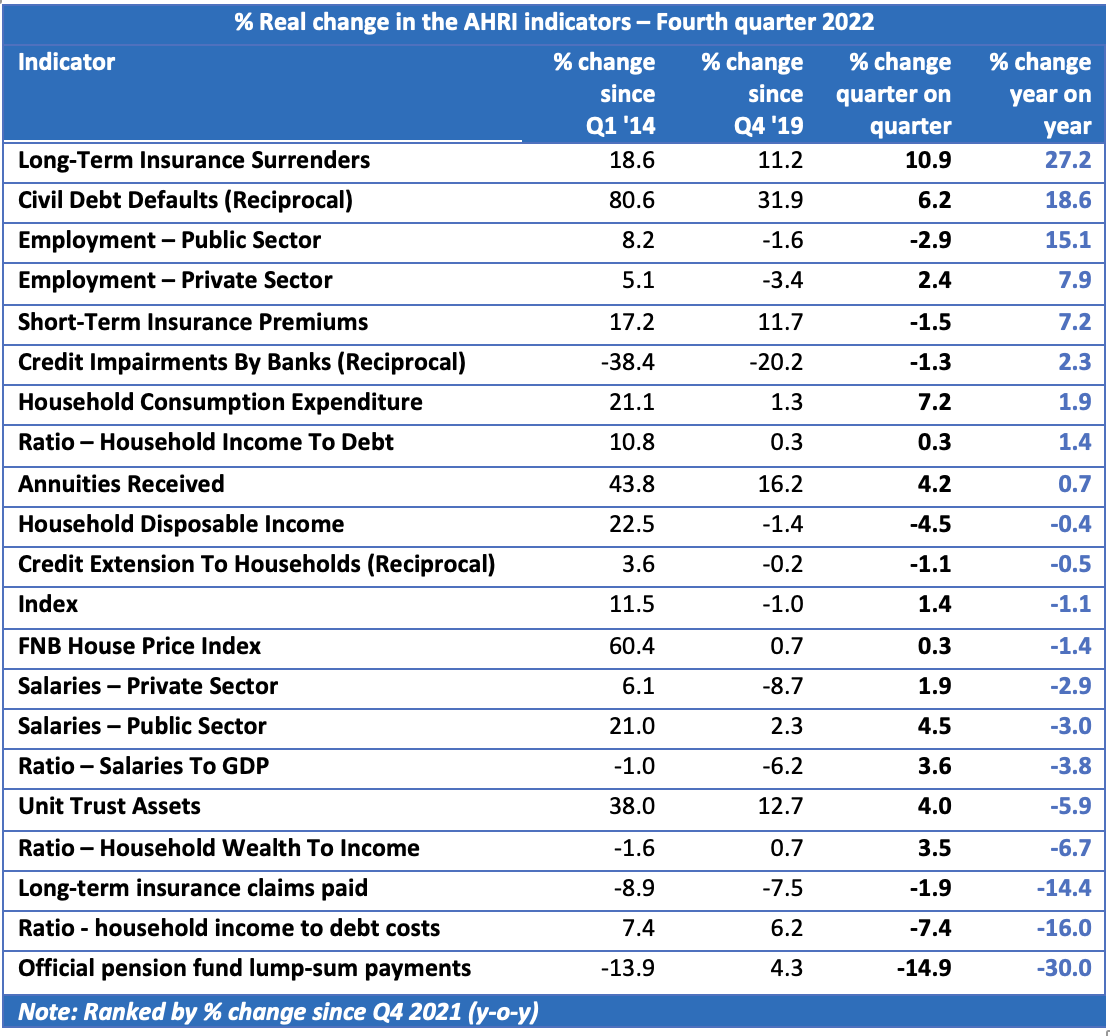

The table below summarises the performance of the different indicators comprising the AFHRI over four different periods: since the base period (2014); since the last comparable quarter before the COVID-19 lockdowns kicked in (Q4 2019); and both the quarter-on-quarter and year-on-year percentage changes. The period since the fourth quarter of 2019 is regarded as relevant in order to gauge whether the financial resilience of households has fully recovered from the pandemic or not.

“It should be noted that employment and labour remuneration in the public and private sectors enjoy a relatively high weighting in the AFHRI, as these indicators represent the mainstay of the financial disposition of most households,” says DR Botha.

Other key conclusions:

- A further increase in employment in both the private and public sectors represented one of the major reasons for the relative stability in the financial resilience of households. The upward trend in new job creation continued in the fourth quarter of 2022, with almost 1.4 million new jobs having been created in 2022. Unfortunately, this positive effect was diminished by lower levels of remuneration. In real terms, the average monthly remuneration in South Africa has declined by 11.4% over the past year (from R18,470 in the fourth quarter of 2021 to R16,370 in the fourth quarter of 2022). The data refers to the average for both the formal and informal sectors. At the end of 2022, the average monthly salary in the formal non-agricultural sectors was almost 60% higher at R26,000.

- Although household financial resilience was boosted by a substantial increase in surrenders of long-term insurance policies, this trend is not conducive to future financial stability and is a clear sign of the hardship faced by many households as a result of higher inflation, higher interest rates and a low-growth economic environment.

- The reciprocals of civil debt defaults and credit impairments by banks have made a positive contribution to the AFHRI, confirming the inherent stability of South Africa’s banking system and the prudent management of debt by households in general. To a large extent, the latter has been necessitated by the sharp decline in the ratio of household income to debt costs.

- An indictment of the SARB’s interest rate policy is the fact that total household credit extension has not remotely recovered from the effects of the extremely high real interest rates that existed before the pandemic and remains well below the level of a decade ago in real terms.

On this last point, Dr Botha notes that since 1998, the total value of outstanding mortgage advances has declined by more than 10% in real terms.

“The South African economy has never been able to grow at sustainably high rates in the absence of meaningful growth in private sector credit extension. To the extent that unjustified hawkish monetary policy reduces output growth, fiscal stability will also be threatened. Inflation targets are not cast in concrete and the SARB should consider a temporary adjustment from 3-6% to 4-7%. This would immediately allow for a 100 basis point reduction in the repo rate and serve to breathe some life into a stagnant economy.”