MEDIA RELEASE

Altron FinTech Household Resilience Index (AFHRI) Quarter 3 of 2022 released

“Positive features include significant employment gains in the public and private sectors, and a meaningful increase in total household disposable income. Of concern, however, is that household credit extension was lower during the third quarter of 2022 than 10 years ago.”

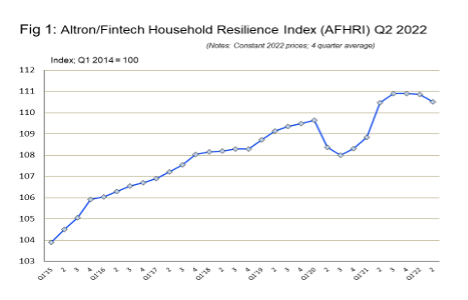

Johannesburg, 18 January 2023 – Altron FinTech today released its latest Household Resilience Index (the “AFHRI”), which covers the third quarter of 2022. After recording a record high in the fourth quarter of 2021, the index took a slight dip in the first and second quarters of 2022, but has bounced back to a level of 109.8, marginally lower than the value of a year earlier.

Due to a traditional spike in the AFHRI during the fourth quarter of each year (due to the shopping boom associated with Black Friday and Christmas), it is useful to examine the four-year average trend.

In the third quarter of 2022, this value was unchanged from the previous quarter (110.5) and only marginally lower than the figure for the previous three quarters (110.9). Since the launch of the AFHRI, the financial resilience of South African households has increased by 9.8% in real terms. The index has fully recovered from the downturn experienced during the COVID-19 pandemic.

In recognition of the need for data that provides more clarity on the financial disposition of households in general, and their ability to cope with debt in particular, Altron FinTech commissioned economist and economic advisor to the Optimum Investment Group, Dr Roelof Botha, to assist in designing this index.

Botha says that the latest quarterly reading of 109.8 is marginally lower than the level of 109.9 recorded in the first quarter of 2022 but 0.6% higher than the second quarter reading.

“Against the background of positive real GDP growth during the third quarter of 2022, the quarter-on-quarter increase was not unexpected. Although the year-on-year Index value recorded a marginal decline of 0.2%, this does not constitute a cause for undue concern, but scrutiny of the trends for the different indicators reveals a more pronounced downward trend for indicators of household wealth.”

According to Botha, the most encouraging features of the latest AFHRI include the significant employment gains in both the public and private sectors of the economy, as well as a meaningful increase in total household disposable income. The latter has become a consistent trend and the disposable income of households is one of only three indicators that has shown growth over all four periods analysed.

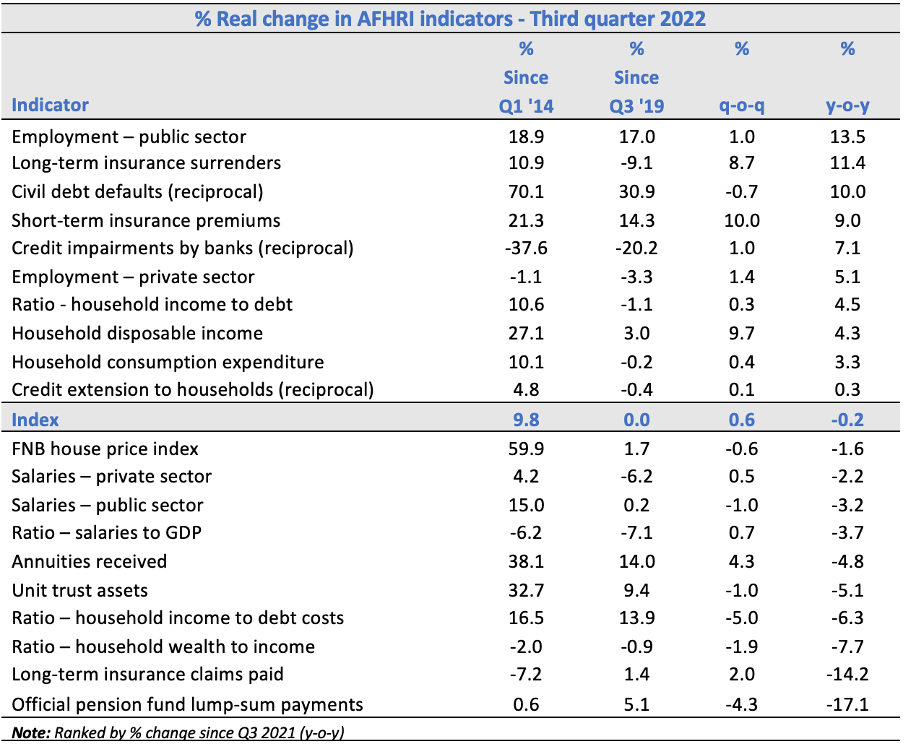

The table below summarises the performance of the 20 different indicators comprising the AFHRI over four different periods, namely since the base period (2014); since the last comparable quarter before the COVID-19 lockdowns kicked in (Q3 2019); and quarter-on-quarter and year-on-year percentage changes.

The period since the third quarter of 2019 is regarded as relevant, in order to gauge whether the financial resilience of households has fully recovered from the pandemic.

Botha says the AFHRI trend line shows broad similarity with a number of other key economic indicators, including GDP and retail trade sales. “It should be noted that employment and labour remuneration in the public and private sectors enjoy a relatively high weighting in the AFHRI, as these indicators represent the mainstay of the financial disposition of most households.”

Key conclusions:

- The performance of the AFHRI since the onset of the COVID-19 pandemic has lagged behind that of the economy as a whole, but only marginally so. During the third quarter of 2022, the AFHRI returned to the same level as the comparable pre-COVID-19 quarter (i.e., the third quarter of 2019). Over this period, real GDP growth was only marginally better at 1.1%, a performance made possible in large part by record exports in 2021 and 2022.

- A significant increase in employment in both the private and public sectors represented one of the major reasons for the continued stability in the financial resilience of households. The upward trend in new job creation continued unabated in the third quarter of 2022, with the total number of formal sector employment rising by more than one million during the first nine months of the year. Although more muted than during the first two quarters of the year, another 235,000 new formal sector jobs were created between July and September 2022. Total employment has increased from 14.3 million a year ago to almost 15.8 million.

- The fact that neither private sector salaries nor public sector salaries were able to record positive real growth in the third quarter may be attributed to three factors: a traditional lag between employment creation and the first payday; inadequate capturing of informal sector remuneration by Statistics SA; and many new workers being prepared to work for more modest salaries.

- The reciprocal of credit impairments by banks has made a welcome return to a positive contribution to the AFHRI, confirming the inherent stability of South Africa’s banking system and the lower default risk emanating from significant new job creation.

- Although the ratio of household income to debt costs has improved considerably since pre-COVID, relatively high negative quarter-on-quarter and year-on-year readings were recorded during the third quarter. With interest rates likely to rise further during the first half of 2023, this indicator is expected to weigh on the AFHRI until the South African Reserve Bank reverses its unduly restrictive monetary policy stance.

- The negative quarter-on-quarter and year-on-year readings for unit trust assets can be attributed to the general weakness of global equity markets over the past year, mainly as a result of the US Federal Reserve having raised its benchmark interest rate from zero in March 2020 to a range of 4.25% to 4.5% at the end of 2022. Together with the weakness of the Chinese economy and heightened geo-political uncertainty in Eastern Europe, this has prompted a fairly prolonged risk-off sentiment amongst most global fund managers. Due to inflation having peaked in most countries, including the US, equity markets rebounded strongly during the fourth quarter of 2022 and this trend is expected to have a positive impact on the next AFHRI reading.

- The South African macro-economy remains in good shape, as witnessed, inter alia, by positive GDP growth in the third quarter, the resilience of the AFHRI, the strengthening of the rand exchange rate and record export earnings in 2022. It remains to be seen, however, whether government can succeed in reversing the general downbeat mood amongst consumers, due mainly to the escalation of electricity rationing, decaying roads, high fuel prices, and higher inflation and interest rates.

- A point of particular concern is the fact that household credit extension was lower during the third quarter of 2022 than ten years ago (in real terms). This is a clear indication that the high cost of credit and of capital in South Africa is curtailing the country’s growth potential.

- Despite formidable obstacles to economic growth, it is highly likely that the AFHRI will continue its upward momentum during the fourth quarter, mainly as a result of the traditional spike in retail trade sales during November and December of each year.

According to the MD of Altron FinTech Johan Gellatly, the AFHRI, along with the Altron FinTech Short-term Credit Impact (AFSCI) Index, generates valuable information that provides the company with a steer on expected market trends.

“Our clients look to Altron FinTech to be a thought leader in the markets we serve, and to incorporate our deep knowledge and experience into our products and solutions to enable them to take full advantage of prevailing economic conditions, both positive and negative. In addition, the index continues to inform key players in our industry, a real necessity in today’s business climate.”

Gellatly says that as the index improves, so does the ability to service debt, and it is of the utmost importance to have solutions that assist businesses to both lend and collect successfully. “The solutions that Altron FinTech provides within the unsecured lending space include loan management and integrated collection solutions to ensure our customers in this industry are best placed to manage their customers and lending books effectively.”

Every month Altron FinTech registers 530,000 new loans via the South African Credit and Risk Reporting Association (SACRRA) and completes 425,000 credit checks for affordability assessments as part of its regulatory compliance.

“We also assist our customers to manage 2.2 million credit agreements by updating their payment profiles on a monthly basis, and process more than 2.6 million transactions, amounting to more than R2.5 billion in successful collections, each month for our customers. This helps ensure healthy collection rates.”